Map the gamma

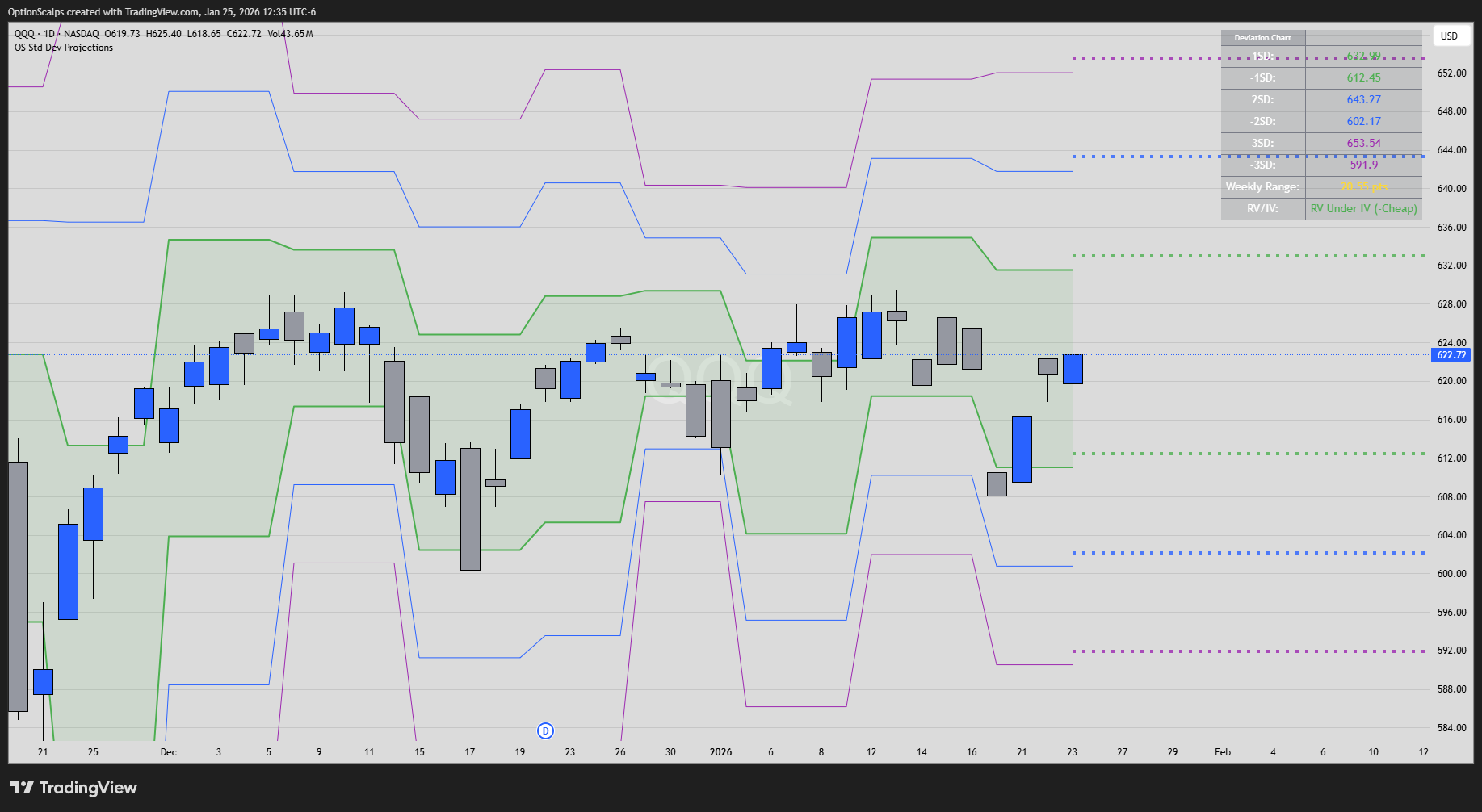

Before the open we chart dealer exposure across strikes — gamma, charm and vanna — to find levels where hedging flow pins price or accelerates it. How that works.

Est. 2023 · Corvallis, Oregon

Rawstocks is an options desk. You get the entry, the stop and the target the moment we take a position — and the outcome goes on the record whether it worked or not. Check the record before you pay us anything.

Cancel inside the trial and you are not billed again.

The record

Every closed trade the desk publishes, logged with its percentage result. Losses are not quietly removed — they are the reason this page is worth reading.

| Date | Instrument | Expiry | Result | P/L |

|---|

How the desk trades

No indicators to argue about. We read where dealers are hedged, wait for price to reach a level that matters, and size the position so a wrong read costs a known amount.

Before the open we chart dealer exposure across strikes — gamma, charm and vanna — to find levels where hedging flow pins price or accelerates it. How that works.

A level alone is not a trade. Price has to arrive with a liquidity sweep or an imbalance behind it. Smart Money Concepts, applied to a pre-marked level.

The alert goes out in real time as the position is taken. When it closes, the result goes on the public record at its percentage return — win or loss, no exceptions and no edits afterwards.

Who is actually behind this

Three people, named, with the instruments they actually trade. If you are going to take a position because someone told you to, you should know who told you.

Founded the desk in 2023. Runs the Sunday sessions and most of the TSLA and single-name flow.

Runs the 0DTE and SPX side. Trades a narrow set of levels repeatedly rather than hunting new setups.

[One or two lines on what Gandalf trades and what he contributes to the desk.]

Verified reviews · Whop

Rustik has a very high hit rate and provides real insight. I did not think that was possible in markets this difficult.@VrynH — Premium member

One of the few trading groups that feels legitimate. People share real setups and explain the reasoning instead of just posting entries.Verified purchase — September 2025

If you want to learn gamma, ICT concepts and options flow, this is the place. Patient teaching and detailed analysis every day.Verified purchase — Whop

I am a new trader and the team makes it easy to follow along. Respectful room, members actually share ideas.Verified purchase — September 2025

Membership

Start on the trial. If the record does not hold up over seven days, cancel — that is the entire point of publishing it.

Before you join

It goes on the record the same way a winner does, with the entry, the stop and the exit. We do not delete alerts, and we do not reframe a stopped-out position as a lesson. A desk that only shows you winners is showing you a marketing page, not a track record.

Seven days for $7, with full access — alerts, sessions, scanner and the record. Cancel inside those seven days and you are not billed again. Billing is handled by Whop, not by us.

In real time, posted to Discord as the desk takes the position — not summarised afterwards. When the position closes, its percentage result goes on the public record whether it worked or not.

No. Sunday sessions start from market structure and options mechanics. That said, options can lose their entire value quickly, so start with size you can afford to lose while you learn the desk's rhythm.

Yes. The free Discord and the research blog carry weekly breakdowns and market notes. Premium is where the live alerts, the scanner and the sessions are.

No. We publish what the desk is doing with its own capital and teach the reasoning behind it. We are not registered investment advisers, we do not know your circumstances, and nothing here is a recommendation for you specifically.

Risk disclosure

Trading options involves substantial risk of loss and is not suitable for every investor. Options can expire worthless. It is possible to lose the entire amount paid for a position in a single session.

Rawstocks LLC is a trading education and analysis community. We are not a registered investment adviser or broker-dealer, and nothing published here constitutes personalized investment advice. Past performance does not indicate future results. Read the full disclosure.

Seven days, seven dollars

You do not have to trust us. Check the tape, sit in for a week, and see whether the levels hold up in a live session.

Start the 7-day trial — $7